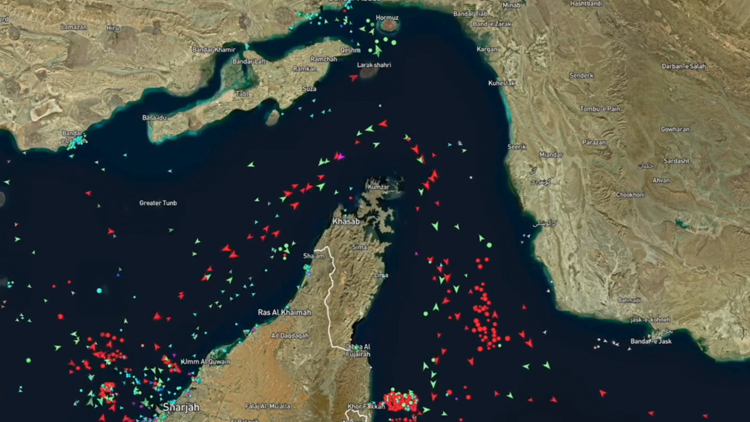

What Happened?

The recent U.S.–Israel war with Iran has disrupted shipping through the Strait of Hormuz, immediately exposing a long-standing structural weakness in Iraq's oil export system. Nearly 93% of Iraq's crude exports flow through Basra's export infrastructure, which is wholly dependent on uninterrupted Gulf access.1 With oil exports averaging around 3.26 million barrels per day (bpd) at roughly 68 USD per barrel in the month before the war, a full disruption would cost Iraq about 221 million USD in daily revenue. This is a sobering figure given that oil accounts for nearly 90% of federal state revenues.2

Why It Happened?

Iraq's export geography has not meaningfully changed in decades. The majority of Iraq’s exports flow through the Persian Gulf from the al-Basrah Oil Terminal and several single point moorings. Alternative corridors, including the Iraqi Pipeline in Saudi Arabia (IPSA) to the Red Sea, the Iraq-Syria Pipeline through Syria to the Mediterranean, and the Iraq–Turkey Pipeline (ITP), were all developed in the 1970s and 1980s. Jordan and Iraq have been discussing the potential for an Iraq-Jordan pipeline since 2013, but this remains a concept on paper. Today, only the ITP remains nominally active, with actual export of around 250,000 bpd against a nameplate capacity of 1,600,000 bpd. However, it is constrained by infrastructure deterioration, production-decline in northern fields, and regional instability. The other routes have fallen into disuse through a combination of physical degradation, unresolved political disputes, and shifting regional alignments.

Why It Matters for Iraq?

Export concentration is not merely a logistical problem with substantial economic and fiscal implications. The northern corridor could theoretically have moved 400,000–500,000 bpd, but security uncertainty and the unresolved Baghdad–Erbil dispute delayed any export resumption for nearly 18 days after the Strait of Hormuz was closed. The absence of credible security guarantees for international oil companies operating in the Kurdistan Region has kept an additional 200,000 bpd effectively stranded. Iraq's relationships with the countries that could unlock alternative routes — Saudi Arabia, Jordan, and Syria continue to be complicated by domestic political pressures that have historically obstructed normal bilateral engagement.

What to Watch for Next

As long as the current crisis endures, Iraq will suffer financially. The new Iraqi cabinet will need to determine if it will prioritize serious infrastructure investment. Iraq is well aware of the policy and technical discussions regarding export diversification. The question is whether institutional inertia, fiscal constraints, investor confidence, and the political economy of sectarian populism will once again prevent the government from acting on a lesson it has already paid to learn.